The baseball player Yogi Berra once said that “a nickel ain’t worth a dime anymore.” With inflation still elevated, many investors and consumers may be feeling this way as well. Not only are everyday costs higher due to energy prices, but short-term interest rates have fallen over the past two years.

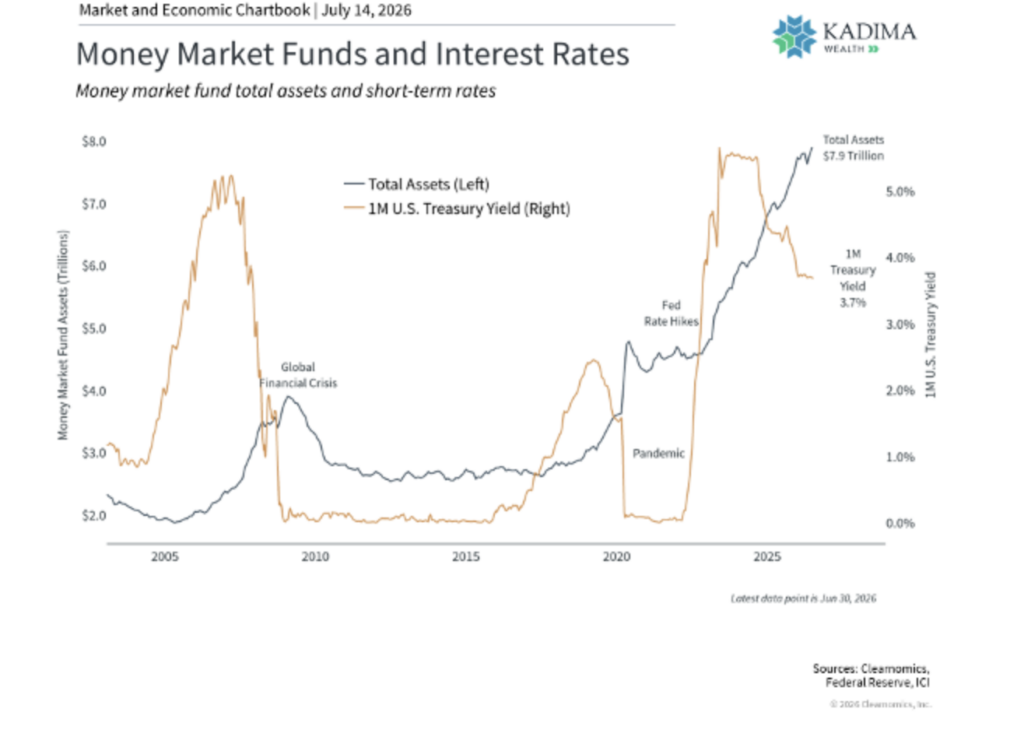

Investors who hold a significant portion of their portfolios in cash are seeing the purchasing power of their savings erode on two fronts: rising prices and declining cash yields. With money market fund assets near record highs at $7.9 trillion, it is likely that many investors maintain cash allocations that exceed what is appropriate for their financial plans.1 So what should investors understand about the role of cash in their portfolios today?

Managing cash requires careful planning

Cash serves many purposes across portfolios, financial plans, and everyday life, making it a nuanced topic. Holding too much of it, however, carries real long-term costs that are easy to overlook. Cash feels safe, particularly when compared to the daily volatility of the stock market, yet history demonstrates that excessive cash holdings can create a drag on wealth accumulation

From an investing and financial planning perspective, the term “cash” broadly refers to any liquid, short-term holding or vehicle. Common examples include savings accounts, money market funds, certificates of deposit (CDs), and similar instruments. These tools serve important purposes such as covering near-term expenses, building an emergency fund, saving for a home down payment, or setting aside money for tuition payments. Each of these represents a legitimate and necessary use of cash within any financial plan.

The key question is not whether to hold cash, but how much is appropriate given an individual’s goals, time horizon, and overall portfolio. Excess cash is sometimes referred to as ‘cash on the sidelines,’ as it is generally not participating in the long-term growth potential associated with stocks or the income potential available from longer-term investments.

As the accompanying chart shows, money market fund assets remain at record levels after climbing alongside interest rates a few years ago. Higher short-term interest rates can appear attractive, especially when the stock market seems volatile. Because these rates are short-term in nature, they are not locked in, creating what investors often refer to as “reinvestment risk.” To help preserve purchasing power and support long-term financial goals, investors should evaluate whether excess cash could be more effectively allocated to investments that align with their objectives, time horizon, and risk tolerance.

This concern is especially relevant today, since short-term rates have already declined. Investors who increased their cash allocations may have experienced lower yields and, depending on when they shifted to cash, may have missed some of the broader market rally over the past few years.

Inflation quietly erodes the value of cash

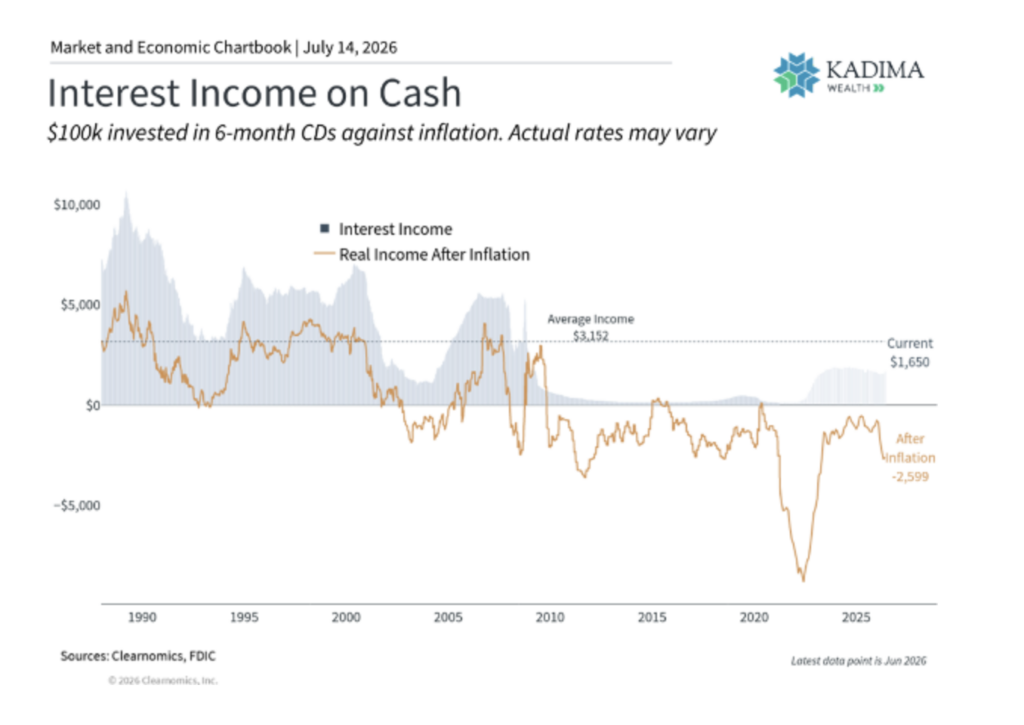

A common misconception is that cash is truly risk-free. While the nominal balance on a bank statement does not fluctuate the way the stock market does, the true value of cash can decline all the same. The purchasing power of cash is eroded by inflation over time. This inflationary effect may appear small in any given year, but it compounds across years and decades unless interest payments or asset appreciation offset it.

As the chart above shows, the inflation-adjusted return on cash, measured using current CD rates according to the FDIC, has been negative for most of the past two decades.2 In other words, even when cash appeared to be generating some income, inflation was running ahead of it. With headline inflation currently at 4.2% and the one-month Treasury yield at 3.7%, real cash yields remain negative today by many measures.3

Money market funds, savings accounts, and short-term CDs must be rolled over regularly as they mature. This reinvestment risk not only needs to be actively managed, but is also subject to shifting market and economic conditions. As a result, many of the same factors that affect stocks and bonds also influence the yields available on cash.

Stocks and bonds support long-term growth

Stocks and bonds have traditionally served as the foundation of portfolios because they can generate both long-term growth and income. Dividend-paying stocks, for instance, can provide income alongside the potential for capital appreciation. While dividend payments are not guaranteed and may be increased, reduced, or eliminated, bond coupon payments are contractual obligations of the issuer but remain subject to the issuer’s ability to make timely payments.

Extending the maturity on bonds can also result in more attractive interest rates. The 2-year Treasury yield is currently around 4.2%, which represents both a significant increase over short-term cash yields and also aligns with the latest inflation figures. Investment grade corporate bonds currently yield 5.3% on average, compared to a historical level of 3.9%. The Bloomberg U.S. Aggregate Bond Index yields 4.8%, more than one and a half times its average since 2009. Unlike cash, bonds can also gain in value, particularly in ways that may complement the broader portfolio.

Ultimately, history shows that a portfolio with the right mix of asset classes can not only outpace inflation over time, but can compound to support long-term financial goals. This is not an argument against holding cash, but rather a reminder that the purpose of cash in a portfolio is to address specific, near-term needs. For investors who have accumulated excess cash over the past few years, putting it to work in a thoughtful manner is an important step forward.

The bottom line? Cash plays an important role in financial planning, but holding too much comes with long-term trade-offs. Staying invested in a diversified portfolio of stocks, bonds, cash and other assets has historically been an effective way to work toward long-term financial goals.

References

1. https://www.ici.org/research/stats/mmf

2. https://www.fdic.gov/national-rates-and-rate-caps

3. https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

This material is provided for informational and educational purposes only. The information contained herein is not intended and should not be construed as individualized advice or a recommendation of any kind. Any opinions or forward-looking statements expressed herein are subject to change without notice. The information contained herein has been obtained from sources believed to be reliable but is not necessarily complete, and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein.

Historical market trends are not guarantees of future results, and future market conditions may differ materially from those discussed herein. Current yields and interest rates are subject to change and may not be representative of future market conditions.

Investing involves risk, including the possible loss of principal. Stocks are subject to market risk, and dividend payments are not guaranteed and may be reduced or eliminated. Bonds are subject to interest rate risk, credit risk, inflation risk, and issuer default risk. Bond prices generally decline when interest rates rise. Money market funds seek to maintain a stable net asset value but are not guaranteed or insured by the FDIC or any other government agency, and it is possible to lose money by investing in a money market fund. Certificates of deposit are generally subject to early withdrawal penalties and, while eligible deposits may be protected by FDIC insurance up to applicable limits, they may not keep pace with inflation. Diversification does not ensure a profit or protect against loss in declining markets. There is no guarantee that any investment strategy will achieve its objectives or produce positive returns.